Cobalt 2026

Supply Deficits, AI-Driven Battery Demand Surge, and the Medium-Term Rebalancing

Published 1-May-2026

Cobalt remains one of the most geopolitically sensitive and strategically vital transition metals in the global economy. As of April 2026, the market operates under a structural deficit, with refined availability constrained by policy interventions, logistical frictions, and cascading energy-cost pressures. Prices have stabilized in a elevated bullish range after a dramatic 2025 recovery, while demand (anchored in lithium-ion batteries) receives an additional structural tailwind from the explosive power requirements of AI data centers and grid-scale energy storage. This expanded analysis dissects cobalt as a raw commodity and its downstream transformations, provides granular supply-demand balances across key product streams, evaluates price dynamics (including the indirect but material influence of the 2026 Iran conflict), maps network-level propagation of shocks, and delivers layered short- and medium-term outlooks. Insights draw from primary industry benchmarks, real-time pricing platforms, and analyst consensus as of late April 2026.

Cobalt as a Commodity

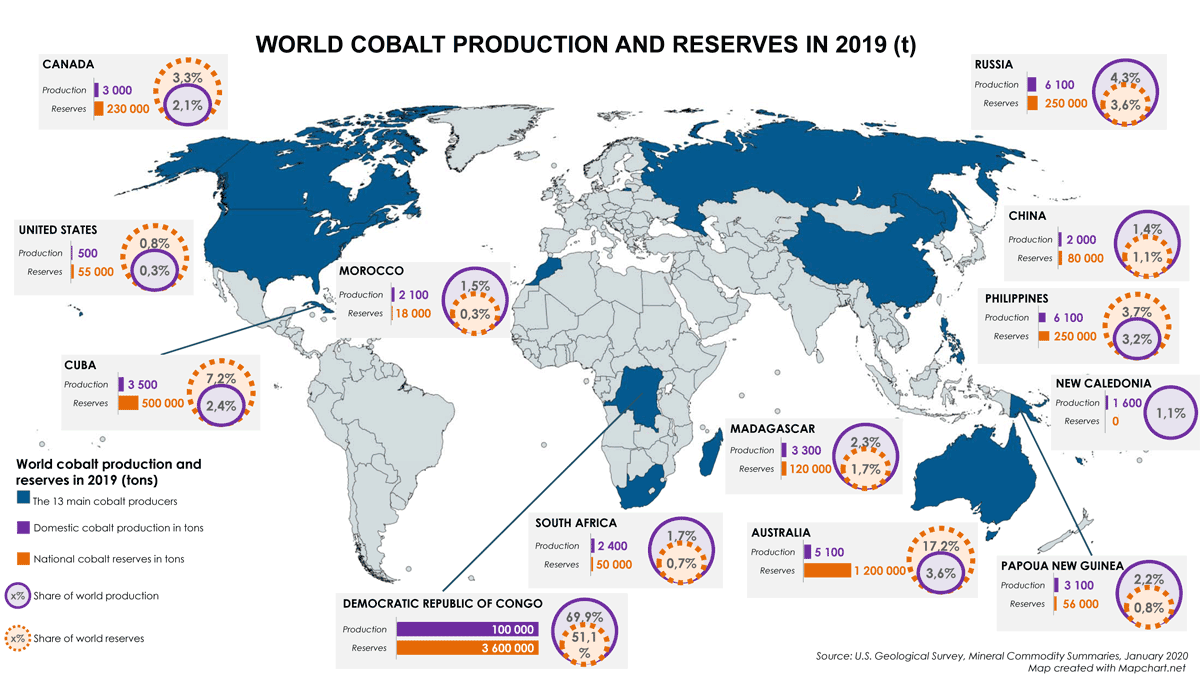

Cobalt (Co, atomic number 27) is a lustrous, silvery-blue, ferromagnetic transition metal prized for its high melting point (1,495 °C), corrosion resistance, and ability to form stable complexes. It is almost never mined in isolation; globally, ~71 % originates as a byproduct of copper-cobalt oxide/sulfide ores, ~22 % from nickel-cobalt laterite/sulfide deposits, and the balance from recycling or polymetallic sources. Major reserves are concentrated in the Democratic Republic of Congo (DRC, >50 % of known resources), followed by Australia, Indonesia, Russia, and Canada.

{kind=link}

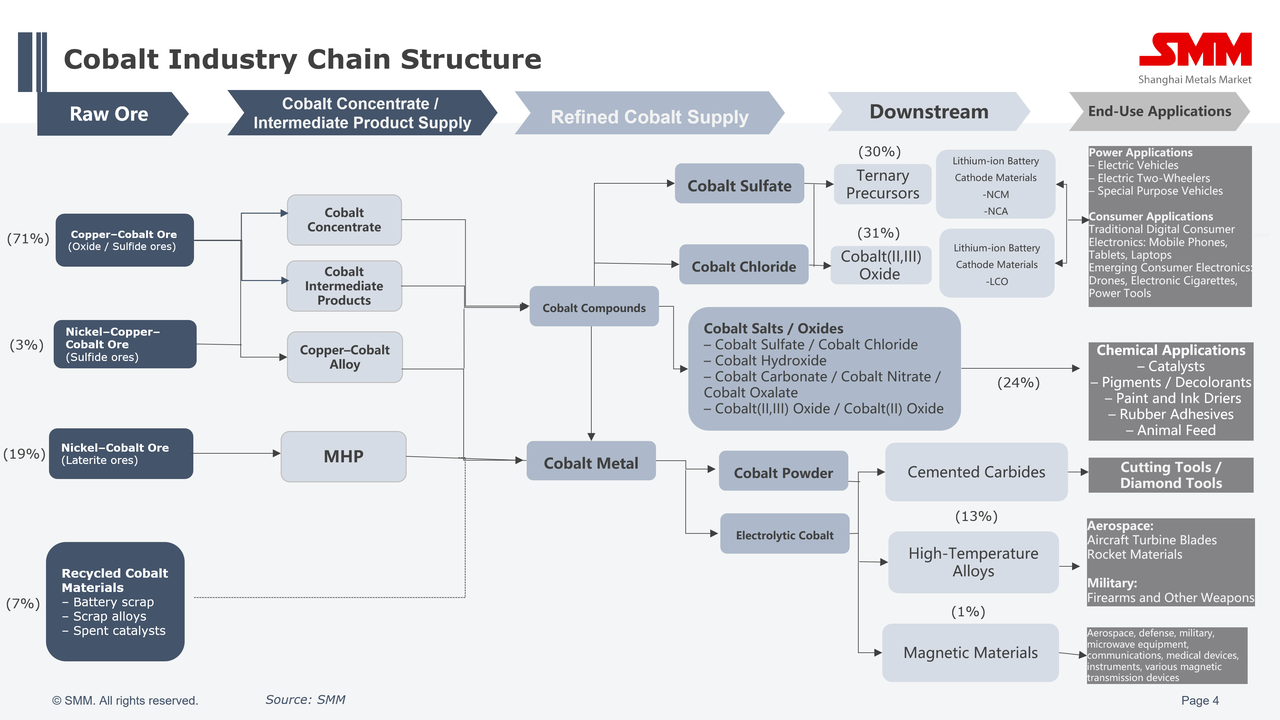

The primary transformation pathway is multi-stage and capital-intensive:

Mining and Concentration: Ores are extracted (open-pit or underground) and beneficiated into concentrates (typically 5–20 % Co) or mixed hydroxide precipitate (MHP, ~30–40 % Ni + Co) via high-pressure acid leaching (HPAL) in the case of Indonesian nickel laterites.

Intermediate Processing: Concentrates undergo leaching (sulfuric acid), solvent extraction, and precipitation to yield cobalt hydroxide, carbonate, or sulfate intermediates.

Refining: Predominantly in China (~80–85 % of global capacity), intermediates are converted via hydrometallurgy into:

Battery-grade cobalt sulfate (~46–50 % of refined output): High-purity (>99.9 %) crystals produced by dissolving hydroxide in sulfuric acid followed by crystallization. This is the direct feedstock for nickel-manganese-cobalt (NMC) and nickel-cobalt-aluminum (NCA) cathode precursors in lithium-ion batteries.

Cobalt oxides and salts (chloride, carbonate, nitrate): Used in lithium cobalt oxide (LCO) cathodes for consumer electronics, pigments, glass, ceramics, and petrochemical catalysts.

Cobalt metal and powder: Electrolytic deposition or hydrogen reduction yields cathode-grade metal (99.8 %+) for superalloys (aerospace turbine blades), cemented carbides (cutting tools), and magnetic alloys.

{kind=link}

Downstream specialized industries and direct commodity-to-product linkages:

Battery sector (70 %+ of total use): Sulfate is non-substitutable in premium high-energy-density chemistries; even with declining cobalt intensity per kWh (from ~150 g/kWh in 2020 NMC 811 to <80 g/kWh in newer designs), absolute volume demand grows with battery gigafactory buildout.

Aerospace and defense (13 %+): Cobalt-based superalloys (e.g., Haynes 188, Rene 41) provide creep resistance at >1,000 °C in jet engines and gas turbines.

Hard metals and tooling: Cobalt binds tungsten carbide in drill bits and wear parts.

Chemicals and pigments: Oxides deliver vibrant blues in glass, ceramics, and paints; catalysts accelerate Fischer-Tropsch and hydrodesulfurization reactions.

Recycling loop: Black-mass hydrometallurgy from spent EV batteries and electronics now supplies ~7–10 % of refined cobalt, with collection rates rising but still limited by logistics and economics.

These streams are not fully fungible; reprocessing sulfate back to metal or vice-versa incurs 10–20 % yield losses and added costs, creating distinct market segments with their own supply-demand elasticities.

Supply Landscape: Policy Caps, Ramp-Ups, and Persistent Bottlenecks (April 2026)

Global mined production is tracking toward ~310–350 kt cobalt content in 2026, yet effective refined supply reaching the market is materially tighter.

DRC (73–76 % share): Output ~260–270 kt mined equivalent, but the February 2025 export suspension was replaced by a formal hydroxide quota of 96,600 t for 2026–2027 (including a 9,600 t strategic reserve). Actual Q1–Q2 shipments have lagged due to port congestion, mandatory testing protocols, and inland logistics, creating an ex-DRC market deficit estimated at ~50–53 kt in effective availability.

Indonesia (rapid riser, ~14–17 % share): Production reached ~38 kt in 2025 and is forecast to climb 39 % to ~53 kt in 2026, driven by Chinese-backed HPAL projects (e.g., Huafei, Halmahera). However, upstream nickel ore curtailments and sulfuric-acid feedstock volatility constrain full utilization.

Other producers: Australia, Canada, Russia, and Madagascar contribute marginal but stable tonnes; secondary/recycled supply grows fastest (~10 % CAGR) but remains <20 % of total.

Refining chokepoint: China dominates chemical conversion; stocks reportedly reached critically low levels by early 2026, amplifying squeeze risks despite nominal mine output growth.

Overall, supply is policy-constrained at source and logistically fragile, preventing full quota utilization and keeping physical markets tight.

Demand: Battery Resilience Meets AI/Electricity-Driven Acceleration (April 2026)

Refined cobalt demand is projected at ~219–220 kt in 2026 (7 % YoY growth after a softer 3 % in 2025), with batteries accounting for ~70 %+.

EV and portable electronics: Core volume driver, though cobalt intensity per kWh continues modest decline. LCO cathodes remain resilient in smartphones and laptops.

Energy storage systems (BESS/ESS): The AI-electricity nexus is a structural game-changer. Hyperscale data centers (projected to add hundreds of TWh of power demand by 2030) require reliable backup and peak-shaving storage; many operators fast-track lithium-ion BESS deployments, directly lifting sulfate consumption beyond traditional EV forecasts.

Superalloys and industrial uses: Aerospace/defense demand steady at 13 %+, supported by commercial aviation recovery and military spending. Catalysts, magnets, and hard metals provide diversification.

Nuances and edge cases: High prices trigger partial substitution (LFP in mass-market EVs and some stationary storage), yet premium segments (long-range EVs, high-cycle BESS, aerospace) exhibit low elasticity. Demand destruction risk is limited in strategic applications; long-term contracts and strategic stockpiling by battery makers further insulate volumes.

The interplay of electrification and AI power hunger creates a dual-tailwind dynamic that offsets softer EV outlooks in certain regions.

Price Analysis: From 2025 Oversupply Fears to 2026 Structural Tightness

Cobalt metal (LME standard grade) has traded in a $56,000–62,000/t range through Q1 2026, closing near $56,290/t as of late April—flat month-on-month but up ~67 % year-over-year from 2025 lows. Hydroxide and sulfate followed similar trajectories, with earlier spikes (hydroxide +263 % peak-to-trough in 2025) and persistent battery-grade premiums driven by ESG traceability requirements.

Historical context and recent drivers (graph below illustrates the dramatic 2025–2026 reversal):

Prices recovered on DRC policy shocks rather than pure demand explosion, but the subsequent inventory drawdown and energy-cost inflation have embedded a higher floor. Premiums for ex-DRC material and traceable sulfate reflect buyer willingness to pay for supply certainty amid quota uncertainty.

The 2026 Iran Conflict: Indirect but Material Geopolitical Amplifiers

Although cobalt is not mined in the Middle East, the escalation of the Iran conflict (U.S./Israel strikes from February 2026 onward) has transmitted second- and third-order shocks through energy, chemicals, and logistics channels.

Energy and freight inflation: Oil prices exceeding $100–110/bbl raised diesel and electricity costs for energy-intensive HPAL operations in Indonesia and DRC leaching/smelting, squeezing margins and slowing ramp-ups.

Sulfuric acid and sulfur feedstock crisis: Gulf sulfur production (critical for acid used in cobalt refining and nickel HPAL) faced disruptions, elevating chemical input costs and constraining Indonesian intermediate output.

Logistics and insurance: Strait of Hormuz volatility forced rerouting, higher war-risk premiums, and port delays, inflating delivered costs for Asian and European buyers.

Strategic metal scramble: Heightened defense spending and U.S. reserve initiatives increased cobalt offtake for aerospace and electronics, while AI operators accelerated BESS procurement amid power-security concerns.

These effects interacted multiplicatively with DRC quotas, accelerating the shift from balance to deficit faster than baseline models anticipated.

Network Analysis: First-, Second-, and Higher-Order Shock Propagation

The cobalt value chain is a highly concentrated, multi-node network with low redundancy.

First-order (direct) effects:

Iran → immediate energy/sulfur/logistics cost spikes → margin compression in HPAL and DRC processing → delayed output.

DRC quotas → physical tightness → spot premiums.

Second-order effects:

Cost pressure → slower Indonesia ramps and potential production curtailments.

Price surge → accelerated long-term contracting and strategic stockpiling → further inventory drawdown.

AI BESS urgency → demand resilience despite elevated prices.

Higher-order (third+) effects:

Supply-chain reconfiguration: Accelerated Western investment in non-China refining (Lobito Corridor, North American projects) and recycling scale-up.

Policy feedback: Possible DRC quota adjustments; export restrictions elsewhere; widening ESG premiums.

Macro rebound: Elevated energy costs may temper global growth (partial demand offset), while defense/aerospace budgets rise.

Systemic resilience gains: Reduced single-country concentration risk, albeit at higher short-term costs and volatility. Social risks (artisanal mining in DRC) may intensify if high prices incentivize lower-standard output.

The network’s fragility stems from chokepoints at mining origin, refining concentration, and energy/chemical inputs.

Short-Term Outlook (Q2–Q4 2026): Tightness with Volatility

A ~10 kt+ market deficit persists. Prices are likely to hold $55k–65k/t, with upside risk on any renewed logistics disruptions or further AI-driven BESS tenders. Q1–Q2 DRC shipment normalization could provide modest relief, yet Iran-related cost and freight pressures, combined with resilient battery offtake, maintain a firm floor. Demand destruction remains low-probability in core segments; superalloys stay stable.

Medium-Term Outlook (2027–2030): Rebalancing at Elevated Price Levels

Deficits narrow but do not fully disappear through the decade. Indonesia + recycling growth (secondary supply potentially reaching 39–82 kt by 2030–2040) and new projects gradually ease pressure, while declining cobalt intensity in batteries caps absolute demand growth. Prices should stabilize in a higher base-case range (~$40–50k/t) compared with pre-2025 levels, with an embedded geopolitical risk premium. Key swing factors include DRC policy compliance, full HPAL utilization, recycling economics, and post-conflict energy stability. Diversification policies and U.S./allied reserve builds mitigate (but do not eliminate) concentration risks.

Conclusion

The cobalt market in 2026 exemplifies the tension between the energy transition’s ambitions and the realities of concentrated supply chains, policy intervention, and geopolitical spillover. Structural deficits, amplified by the Iran conflict’s energy and logistics shocks, have lifted prices and incentivized diversification, yet the AI-electricity demand surge ensures cobalt’s enduring role in high-performance batteries and advanced manufacturing. Stakeholders (battery makers, OEMs, miners, and governments) must prioritize traceability, recycling scale-up, and allied refining capacity to build resilience. While short-term volatility is likely, the medium-term trajectory points to a rebalanced but permanently higher-cost market that rewards agility, innovation in substitution where feasible, and long-term supply security. Cobalt’s crossroads status underscores a broader truth: the clean-energy future is inextricably linked to responsible resource stewardship and geopolitical foresight.

Sources

Cobalt Institute – Quarterly Cobalt Market Report Q4 2025: https://www.cobaltinstitute.org/wp-content/uploads/2026/02/Cobalt-Market-Report-Q4-2025.pdf

Metals-Hub – “Cobalt Market: Supply, Demand, & Price Discovery” (25 March 2026): https://www.metals-hub.com/en/blog/cobalt-market-dynamics/

Fastmarkets – “Dried-up feedstock pipeline sends cobalt prices soaring” (6 January 2026): https://www.fastmarkets.com/insights/dried-up-feedstock-pipeline-cobalt-prices-soaring-2025-deficit/

AZoMining – “The Cobalt Market: Key Trends in 2026” (23 April 2026): https://www.azomining.com/Article.aspx?ArticleID=1943

Investing News Network (INN) – “Cobalt Market Forecast 2026”: https://investingnews.com/daily/resource-investing/battery-metals-investing/cobalt-investing/cobalt-forecast/

Trading Economics – Cobalt Price (updated 30 April 2026): https://tradingeconomics.com/commodity/cobalt

Benchmark Mineral Intelligence – “Supply strains keep prices steady: Cobalt Q1 2026 Price Review”: https://source.benchmarkminerals.com/article/supply-strains-keep-prices-steady-cobalt-q1-2026-price-review

Mysteel – “Cobalt Market Enters Transition Year in 2026”: https://www.mysteel.net/analysis/5112557-cobalt-market-enters-transition-year-in-2026-supply-demand-recalibration-to-reshape-price-premiums-and-margins

Mordor Intelligence – Cobalt Market Size, Share & Growth Analysis Report 2026-2031: https://www.mordorintelligence.com/industry-reports/cobalt-market

Grand View Research – Global Cobalt Market Outlook 2025-2030: https://www.grandviewresearch.com/horizon/outlook/cobalt-market-size/global

Additional geopolitical analysis: S&P Global Commodity Insights and IEEFA reports on Middle East energy disruptions (2026): https://www.spglobal.com/commodityinsights and https://ieefa.org/

---

**About the Author**

Dr Jose Luis Chavez Calva is an independent international consultant and economist specialising in energy markets, network theory and innovation. He holds a PhD in Economics from the University of Essex and previously served in Mexico’s Secretariat of Finance and Public Credit (SHCP) and as General Coordinator of the Electricity Market at the Energy Regulatory Commission (CRE). He has been an independent advisor for the last 10 years and has more than 18 years of professional experience. He is a recipient of the 2011 National Public Finance Award.

All original ideas are not mine, but all wrong facts are entirely my own. This article is not investment advise.

Full archive of articles: joseluischavezcalva.substack.com